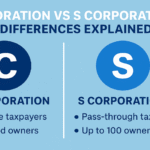

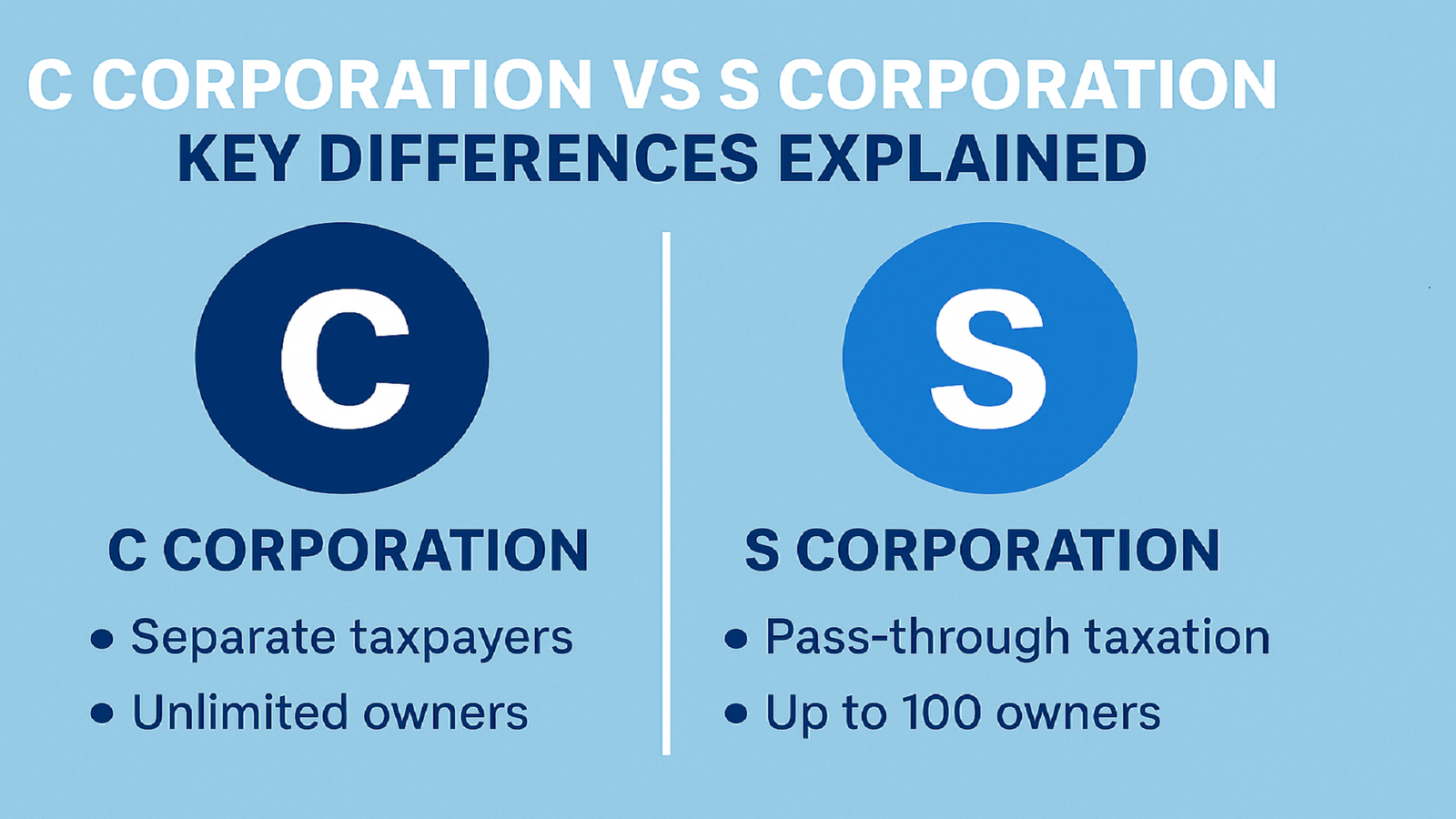

C Corporation vs S Corporation Key Differences Explained is one of the most common questions new business owners ask when deciding how to structure their company. Both options offer liability protection and growth potential, but their tax treatment, ownership rules, and compliance requirements are very different — and understanding these differences can save you time and money from day one.

INTODRUCTION

Running a family business feels different from any other kind of work. It’s not just about profit margins or tax filings — it’s about the long nights where you’re sitting around the dining table talking shop, even when you promised yourself you wouldn’t. It’s about wanting your kids, or maybe even your grandkids, to be proud of what you’ve built. And because the stakes are personal, every choice — even the ones that seem like “boring paperwork” — ends up feeling huge.

One of those choices sneaks up on almost every family business sooner or later: How do we set this up legally? Should we be a C Corporation or make the S Corporation election? At first, it sounds like dry accountant-speak. But here’s the reality: this single decision changes how your profits are taxed, how power is shared in your family, and how easy (or hard) it’ll be to pass the company down when the time comes.

That’s why this guide exists. I want to cut through the jargon, explain what these terms really mean in plain English, and help you figure out which path fits your family’s goals — not just for next year, but for the decades ahead.

C Corporation vs S Corporation Key Differences Explained and What They Mean for Your Family Business

Running a family business is unlike any other challenge. It’s a mix of love, responsibility, and ambition rolled into one. You’re not just building something for profit — you’re building it for your name, for your children, and for the generations that will come after you. That’s why even seemingly “small” decisions — like how to register your company — end up feeling massive.

One of the first crossroads you’ll face is this: Should we form a C Corporation or choose an S Corporation election? On the surface, it looks like an accountant’s problem — something you’ll sign off on without thinking too hard. But here’s the truth: that one choice quietly determines how your profits are taxed, how ownership is shared, and how smoothly your company can pass into the hands of your kids or grandkids when the time comes.

In this guide, we’re going to unpack both options in plain English. I’m not just going to tell you what each one is — I’m going to walk you through how they actually play out for real families. We’ll talk about taxes, control, future growth, and yes, even those family dynamics that can get complicated when business and blood mix.

Let’s Start With the C Corporation

A C Corporation — or C Corp — is the traditional version of a corporation. If you go through the paperwork to incorporate and don’t do anything else, this is what you automatically become. Legally, a C Corp is treated like its own “person.” It can own property, sign contracts, sue or be sued — all without putting the personal assets of its owners at risk.

For a family business, that protection matters more than people realize. Picture this: your family owns a construction company. During a project, something goes wrong — an accident, property damage, maybe even an injury. If you were operating as a simple partnership or sole proprietorship, your family’s house, cars, and savings could all be on the hook. With a C Corporation, liability stops at the business itself. Your personal life stays separate from your professional one.

But legal protection is just one part of the story. C Corporations are built for flexibility and growth. They can have an unlimited number of shareholders. Those shareholders can be individuals, other corporations, even foreign investors. And — this is a big deal for families — they can issue multiple classes of stock. That means you can get creative with who owns what and who gets a say. Maybe the sibling who runs the day-to-day gets voting shares, while the one who lives out of state holds non-voting shares. Everyone benefits financially, but decision-making stays with the people actively managing the company.

Sounds great, right? Here’s the catch: double taxation. C Corporations pay taxes on their profits at the corporate level (currently 21% federally). Then, when they distribute dividends to shareholders, those individuals pay taxes again on their personal returns. For families that rely on regular dividend income, this can sting.

But double taxation isn’t always as bad as it sounds. Many family businesses in their growth phase reinvest most profits instead of distributing them. If you’re using your earnings to buy new equipment, expand locations, or hire staff, the “second tax” might not even come into play until much later. In those cases, the flexibility of a C Corp can outweigh the tax drawback.

READ MORE :https://financebrisk.com/what-is-a-sole-proprietorship/

Investor Appeal and Funding Flexibility:

Another factor families rarely think about early on — but eventually run into — is how investors view their structure. Venture capital firms and angel investors overwhelmingly prefer C Corporations because they can issue preferred shares and handle complex equity arrangements. If your family dreams of building something big enough to attract outside funding someday, setting up as a C Corporation from the beginning can save time and costly restructuring down the road.

Long-Term Tax Planning:

While double taxation is often seen as a disadvantage for C Corporations, it can sometimes work in the family’s favor. The flat 21% corporate rate is lower than many individual tax brackets, especially for high-income families. If most profits are reinvested into the business rather than distributed, the tax savings can compound over time. For families building something that won’t pay out major dividends for years, the C Corp structure can actually reduce their overall tax burden in the long run.

Now, About the S Corporation

An S Corporation — or S Corp — isn’t actually a separate type of company. It’s a tax designation. You start as a regular corporation, but you file an election with the IRS (Form 2553) to be taxed under Subchapter S. This changes how profits are handled — and for many family businesses, it’s a huge relief.

The defining feature of an S Corp is pass-through taxation. Instead of paying corporate income tax, the company’s profits “pass through” directly to the owners’ personal tax returns. The business itself doesn’t pay federal tax at all. If your family-owned bakery makes $200,000 in profit, that money flows straight to the owners and gets taxed just once — at their personal rates.

This setup is ideal for small to medium-sized family businesses that plan to distribute most of their profits each year. It simplifies accounting and often reduces the total tax burden.

But S Corps aren’t perfect. They come with strict rules: no more than 100 shareholders, all shareholders must be U.S. citizens or residents, and you can only issue one class of stock. Everyone gets the same rights to profits and voting. For some families, this equality works well. For others — especially larger families or those wanting to differentiate between active and passive members — it can feel restrictive.

International Ownership Considerations:

Modern families are more spread out than ever. Maybe one of your children lives abroad or marries someone who isn’t a U.S. citizen. In an S Corporation, that’s a problem — foreign shareholders aren’t allowed. A single ineligible owner can accidentally terminate S Corp status and trigger unexpected taxes. A C Corporation, on the other hand, has no such restrictions, making it a safer choice for families with international ties.

Why This Choice Matters So Much for Families

At first, the main difference people focus on is taxes: C Corps pay twice, S Corps pay once. But for family businesses, the bigger question is often about control and flexibility.

C Corporations are great if you envision growth: raising capital, bringing in outside investors, or creating complex ownership plans as your family expands. They let you issue voting and non-voting shares, bring in trusts, and even allow foreign relatives to be shareholders.

S Corporations are perfect if you want to keep things simple: fewer shareholders, equal ownership rights, and profits that flow directly to the family’s pockets without extra tax layers. They’re great for businesses that want to stay small and tightly held.

The Tax Reality: What It Looks Like in Real Life

Let’s break down the tax difference with a simple example.

Imagine your family business earns $500,000 in profit this year.

- As a C Corporation: The company pays 21% corporate tax — that’s $105,000 — leaving $395,000. If you then distribute $200,000 of that as dividends, shareholders pay another 15–20% on those dividends. Total tax hit? Roughly 35% combined.

- As an S Corporation: The $500,000 flows straight to shareholders’ personal returns. No corporate tax. You pay income tax once, based on individual rates. For many families, this ends up lower overall. Plus, S Corp owners who work in the business can split income into salary (subject to payroll tax) and distributions (not subject to self-employment tax), saving even more — if done correctly.

Succession Planning: Passing It Down Without Chaos

Family businesses often dream of being passed down like heirlooms. But succession is tricky — and your corporate structure plays a big role.

C Corporations make succession flexible. Multiple stock classes mean you can design smooth transitions — active children inherit voting shares, passive children inherit non-voting shares, and control stays where it’s needed. Trusts can hold shares easily, making estate planning simpler.

S Corporations are more rigid. They can still work for succession, but you have to be careful: only certain trusts qualify as shareholders, and heirs must remain U.S. individuals. A single ineligible shareholder — say, a relative living abroad — can blow your S status and throw you back into C Corp taxation overnight.

Real Example: The Growing Family Restaurant

Picture a family that owns three local restaurants. In the beginning, profits are modest, and everyone’s equally involved. An S Corporation makes sense — it’s simple, tax-efficient, and fits the close-knit ownership.

But ten years later, the family wants to expand statewide and bring in investors. Suddenly, the S Corp’s limitations — one class of stock, U.S.-only shareholders — don’t fit anymore. They convert to a C Corporation, issue preferred stock to investors, and keep voting control within the family.

Switching Between the Two

The good news? You’re not locked in forever. A C Corporation can become an S Corporation by filing IRS Form 2553. An S Corporation can revoke its status and become a C Corporation if growth demands it. But beware: switching has tax implications, especially if the business has appreciated assets. Always plan conversions carefully with expert advice.

Conclusion: Which Should Your Family Choose?

The choice between C Corporation and S Corporation isn’t just about saving money on taxes. It’s about your family’s vision for the future. Do you see the business staying small and intimate, with profits distributed to family members each year? An S Corporation may be perfect. Do you dream of expansion, outside investors, or complex succession plans? A C Corporation might serve you better.

There’s no one-size-fits-all answer — but there is a right answer for your family. Talk to advisors, map out your goals, and choose the structure that supports not just your business plan, but the legacy you want to leave behind.