What Is Tax Basis and Why Is It Important for My S-Corporation? For many shareholders, tax basis is one of the least understood yet most critical aspects of S-Corp ownership. Your basis determines how much loss you can deduct on your personal return, whether distributions are taxable, and how much gain or loss you’ll recognize when selling your shares. In 2025, with stricter IRS reporting rules like mandatory Form 7203 and increased audit scrutiny, understanding and tracking your tax basis is no longer optional — it’s essential for maximizing deductions, avoiding penalties, and keeping your business compliant.

Introduction For What Is Tax Basis and Why Is It Important for My S-Corporation?

Tax basis is a fundamental concept for S-Corporation shareholders, yet it’s often misunderstood. In simple terms, tax basis represents a shareholder’s investment in the S-Corp for tax purposes. It determines how much of the company’s losses you can deduct, whether distributions are taxable, and how gains or losses are calculated when you sell your shares.

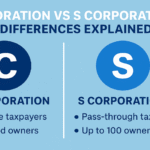

For S-Corporations—which are pass-through entities—income, losses, and deductions flow directly to shareholders’ personal tax returns. However, the IRS imposes strict rules on how these items are treated based on your stock and debt basis. Failing to track basis correctly can lead to unexpected tax liabilities, disallowed deductions, or even IRS audits.

In this 2025 guide, we’ll break down everything you need to know about tax basis, including:

- How stock and debt basis are calculated

- Why basis affects losses, distributions, and capital gains

- Common mistakes and IRS compliance rules

- Practical examples and strategies to maintain accurate records

What Is Tax Basis in an S-Corporation?

Tax basis refers to the amount of your personal investment in the S-Corp that is recognized for tax purposes. Unlike a C-Corporation, where stock basis generally remains fixed unless you buy or sell shares, an S-Corporation’s tax basis changes every year. It adjusts based on the company’s profits, losses, contributions, and distributions — essentially mirroring your financial activity with the company.

Maintaining accurate basis calculations is critical because it dictates how much of the company’s losses you can deduct, whether distributions are taxable, and how capital gains are computed when you sell your stock.

How Tax Basis Works in an S-Corporation

Your tax basis in an S-Corporation is dynamic. It increases when the company earns profits or when you contribute additional capital. Conversely, it decreases when the company experiences losses or when you take distributions. Basis is divided into two main components: stock basis and debt basis.

1. Stock Basis

Your stock basis represents your ownership stake in the S-Corp. It begins with the initial cash or property you contributed when you acquired your shares. Each year, your stock basis must be adjusted to reflect the company’s financial activity reported on Schedule K-1.

Increases to stock basis include:

- Share of profits allocated to you (Box 1 of Schedule K-1)

- Tax-exempt income (e.g., municipal bond interest)

- Additional capital contributions

Decreases to stock basis include:

- Distributions received from the company

- Your share of losses and deductions (operating losses, charitable contributions, etc.)

Example:

Suppose you invest $50,000 to start an S-Corp. In Year 1, the company earns $20,000 in profits, increasing your basis to $70,000. In Year 2, you take a $10,000 distribution, reducing your basis to $60,000.

2. Debt Basis (Loan Basis)

Debt basis arises when you personally lend money to the S-Corporation. This is separate from stock basis and is especially important when the company incurs losses that exceed your stock basis. After your stock basis is reduced to zero, additional losses can only be deducted if you have sufficient debt basis.

Key point:

Debt basis only comes from direct loans you make to the S-Corp. Bank loans guaranteed by you do not count. Additionally, distributions do not affect debt basis — only stock basis matters when withdrawing money.

Important caution:

If the S-Corp repays your loan when your debt basis has been reduced by prior losses, part of that repayment may be taxable income.

Why Tax Basis Matters for S-Corporation Shareholders

Understanding and tracking tax basis isn’t just an accounting exercise — it directly impacts your taxes. Here’s why it’s so crucial:

1. Limits on Loss Deductions

The IRS only allows you to deduct losses up to the amount of your combined stock and debt basis. If the company’s losses exceed your basis, the excess is suspended and carried forward until you restore basis (through future profits or contributions).

Example:

If your stock basis is $30,000 and the company reports a $40,000 loss, you can only deduct $30,000 this year. The remaining $10,000 is suspended until you increase your basis.

2. Tax Treatment of Distributions

Distributions are not automatically tax-free. Their treatment depends on your stock basis at the time of distribution:

- Tax-free: If the distribution is less than your basis, it is treated as a return of capital.

- Taxable: If the distribution exceeds your basis, the excess is taxed as a capital gain.

3. Calculating Capital Gains on Stock Sales

When you sell your S-Corp shares, your gain or loss is determined by subtracting your adjusted basis from the sale price:

Formula:

Sale Price – Adjusted Stock Basis = Capital Gain or Loss

Failing to track basis properly can lead to overstated gains (and overpaid taxes) or understated gains (and potential IRS penalties).

How to Track Tax Basis in 2025

Keeping accurate basis records is your responsibility as a shareholder — the S-Corporation does not provide this information. Here’s how to do it:

- Start with your initial investment. Record the amount of cash or property contributed when you acquired your shares.

- Adjust annually using Schedule K-1. Increase basis for income and decrease it for losses and distributions reported on your K-1.

- File IRS Form 7203. Beginning in 2021, the IRS requires shareholders to file this form when claiming losses, receiving distributions, or selling stock to report basis calculations.

Common Mistakes to Avoid

- Failing to track basis annually: Leads to disallowed loss deductions and IRS penalties.

- Ignoring debt basis: Misses opportunities to deduct losses beyond stock basis.

- Taking distributions without checking basis: Can unexpectedly trigger taxable capital gains.

- Combining traditional and Roth contributions incorrectly: Can cause IRS complications during audits.

Practical Strategies for Maintaining Basis

- Keep a dedicated spreadsheet or use tax software to update basis each year.

- Retain all K-1 forms, contribution records, and loan documents for IRS verification.

- Review basis before making year-end distributions or deducting losses.

- Consult a tax professional annually — basis tracking is one of the most common audit triggers for S-Corporation shareholders.

Why Is Tax Basis Important for S-Corp Shareholders?

Tax basis is one of the most vital calculations for anyone who owns shares in an S-Corporation. It determines how much of the company’s losses you can deduct, whether the distributions you take are taxable, and how much gain or loss you report when you sell your shares. Without accurate basis tracking, shareholders often face disallowed deductions, unexpected tax bills, or even penalties during IRS audits. And with stricter reporting rules taking effect in 2025, maintaining up-to-date basis records is no longer optional — it’s essential for compliance and tax efficiency.

1. The Loss Deduction Firewall

The IRS imposes strict limits on how much loss an S-Corp shareholder can deduct each year, and those limits are based entirely on basis. Specifically, you can only deduct losses up to the total of your stock basis and debt basis combined. Any losses beyond that limit are suspended and carried forward until you restore basis in future years.

For example, if you have a $50,000 basis but your share of company losses is $80,000, you can only deduct $50,000 this year. The remaining $30,000 doesn’t disappear; instead, it becomes a suspended loss that carries forward indefinitely. However, if you never increase your basis — either through additional contributions or future profits — those suspended losses may never become usable, effectively turning them into “phantom deductions” that provide no tax benefit.

2. The Distribution Tax Trap

Basis also determines whether money you take out of the S-Corp is tax-free or taxable. Distributions are considered tax-free returns of capital only to the extent of your stock basis. Once you exceed that basis, the excess amount is treated as a capital gain, which can trigger additional taxes.

Many business owners unknowingly fall into this trap because they fail to track their basis on an annual basis. For instance, if you have a $100,000 basis and you take $120,000 in distributions, the extra $20,000 is taxable as capital gains. Depending on your tax bracket, that could mean paying 15%–20% or more in taxes on funds you assumed were tax-free.

3. The Exit Strategy Tax Bomb

When it comes time to sell your S-Corporation shares, your tax basis plays a critical role in calculating capital gains or losses. The sale gain is determined by subtracting your adjusted basis from the sale price. Underreporting your basis artificially inflates your gain, which means you may pay thousands of dollars in unnecessary taxes.

The IRS is aware of this issue and often scrutinizes basis calculations during audits of business sales. To defend your position, you must provide documentation that traces your basis back to your initial investment, along with annual adjustments for profits, losses, and distributions. Failing to maintain this record can lead to the IRS disallowing your basis claims altogether, leaving you with a much larger tax bill.

READ MORE https://financebrisk.com/what-is-a-sole-proprietorship/

4. The Silent Killer: Debt Basis Complexity

Debt basis rules are another area that trips up many S-Corp shareholders. Unlike stock basis, which arises from your ownership stake, debt basis is created only when you personally lend money directly to the S-Corp. Bank loans or third-party financing that you merely guarantee do not count.

Debt basis is crucial because it allows you to deduct additional losses after your stock basis is depleted. However, there’s a hidden risk: if the S-Corp later repays your loan while your debt basis has been reduced due to prior losses, part of that repayment may be taxable. The order of loss application is also important — losses reduce stock basis first, then debt basis, and only afterward are any excess losses suspended.

5. New 2025 Compliance Requirements

Recent changes to IRS reporting have made basis tracking even more important. Starting in 2021 and continuing into 2025, shareholders must file Form 7203 when claiming losses, taking distributions, or disposing of stock. This form requires detailed calculations and supporting documentation for both stock and debt basis.

The IRS has also heightened scrutiny on compliance, demanding clearer documentation than ever before. To complicate matters further, some states have their own basis rules that differ from federal requirements, creating additional layers of reporting for multi-state taxpayers. These changes make proactive record-keeping and professional guidance essential for avoiding errors and penalties.

How to Calculate and Track S-Corp Tax Basis in 2025

Properly calculating and tracking your S-Corp tax basis is essential for maximizing deductions, avoiding unexpected taxable distributions, and complying with stricter IRS rules introduced in 2025. Many S-Corporation shareholders underestimate the importance of maintaining accurate basis records, but failure to do so can lead to costly mistakes, disallowed losses, and IRS penalties. This detailed guide explains the entire process — from establishing your initial basis to making annual adjustments, tracking loans, and meeting the latest reporting requirements.

1. Start With Your Initial Basis

Your S-Corp tax basis begins the day you acquire your ownership interest. It is calculated using your initial investment, which can include cash contributions, property contributions, or the purchase price of stock. For cash, the calculation is straightforward — it equals the dollar amount you invested. For property contributions, basis equals the fair market value of the property on the date of transfer, minus any liabilities assumed by the corporation. For stock purchases, basis equals the cost of the shares you acquired.

Example:

If you contribute $50,000 in cash and equipment valued at $30,000 to the corporation, and the S-Corp assumes a $10,000 liability associated with the equipment, your starting basis is $70,000 ($50,000 + $30,000 – $10,000). This initial figure serves as the foundation for all future adjustments.

2. Adjust Your Basis Annually Using Schedule K-1

Your tax basis changes every year based on the S-Corp’s financial activity. The IRS requires shareholders to follow a strict order of adjustments when calculating basis annually. First, you must increase your basis for income items, which include ordinary business income reported in Box 1 of your Schedule K-1, as well as separately stated items such as capital gains or tax-exempt income like municipal bond interest.

After increases are applied, you must decrease your basis for distributions, non-deductible expenses, and losses or deductions reported on your K-1. Importantly, losses can never reduce your basis below zero. Any losses that exceed your basis are suspended and carried forward to future years until your basis is restored.

3. Calculate Debt Basis for Shareholder Loans

Debt basis applies only when you personally lend money to the S-Corporation. Bank loans or third-party financing do not create debt basis, even if you personally guarantee them. When you make a direct loan, your debt basis equals the loan amount and increases with additional loans you make. It decreases when the company repays the loan or when losses are allocated to you after your stock basis reaches zero.

A critical caution: if the company repays your loan when your debt basis has been reduced due to prior losses, part of that repayment may be taxable income. Understanding this rule is essential to avoid surprise tax bills when loans are repaid.

4. Maintain Detailed Documentation for 2025

Accurate recordkeeping is essential for proving your basis to the IRS. Maintain capital contribution records, such as bank statements and property appraisals, to substantiate your initial investment. Keep signed promissory notes and repayment schedules for shareholder loans. Retain all Schedule K-1s for at least seven years, as these provide the yearly income, loss, and distribution data required to adjust your basis. Finally, maintain a dedicated basis worksheet or spreadsheet that records your beginning basis, annual increases and decreases, and your ending basis for each tax year.

5. Meet New 2025 IRS Reporting Requirements

Starting in 2025, shareholders must meet stricter IRS reporting rules. If you claim losses, take distributions, or sell shares, you must file Form 7203, which documents your stock and debt basis. This form also requires disclosure of suspended losses from prior years and detailed debt basis calculations. Additionally, be aware that some states have basis rules that differ from federal regulations, requiring separate state-level tracking.

6. Avoid Common Basis Calculation Mistakes

Several mistakes frequently occur when shareholders calculate basis. One of the most common is mixing personal and business loans; only direct shareholder loans to the S-Corp count toward debt basis. Another frequent oversight is ignoring tax-exempt income, which still increases basis even though it is not taxable. Many shareholders also forget to adjust basis for property contributions at fair market value, or fail to account for state-level variations in basis calculations, which can cause discrepancies between federal and state tax filings.

7. Pro Tips for Easier Basis Tracking

To simplify basis tracking, consider using accounting software that supports S-Corp basis calculations, such as QuickBooks with customized basis tracking features. Create an annual basis reconciliation schedule that shows your beginning basis, yearly income allocations, distributions, losses, and ending basis. Reviewing this schedule annually with your CPA ensures accuracy and prevents last-minute surprises during tax filing. For example, a sample reconciliation might show a $100,000 beginning basis, increased by $30,000 of income, reduced by $15,000 of distributions and $5,000 of losses, resulting in a $110,000 ending basis for the year.

7 Common S-Corp Basis Mistakes That Could Cost You in 2025

Even savvy S-Corp owners often make costly basis tracking mistakes that trigger IRS audits and unexpected taxes. These common errors can wipe out deductions and create massive tax bills if left unchecked. Learn how to avoid these pitfalls and protect your S-Corp’s financial health in 2025.

1. The Phantom Basis Trap

One of the most widespread misconceptions is assuming that all business debt automatically increases shareholder basis. In reality, only direct loans from the shareholder to the S-Corporation create debt basis. Bank loans, even if personally guaranteed by the shareholder, do not qualify. This misunderstanding often leads to overstated basis calculations and improper loss deductions. The fix is simple but essential: always document personal loans with signed promissory notes and maintain clear records of repayment terms to ensure they qualify for basis purposes.

2. The Distribution Danger Zone

Distributions from an S-Corp may appear straightforward, but failing to check your basis before taking them can create a tax landmine. When distributions exceed your stock basis, the excess is treated as taxable capital gains rather than tax-free returns of capital. This often happens when owners assume that prior profits automatically cover distributions without calculating annual adjustments. The best practice is to run a basis calculation before every withdrawal to confirm that your distribution falls within tax-free limits and avoid surprise tax bills.

3. The Suspended Losses Black Hole

Another common oversight is neglecting suspended losses from previous years. These losses occur when deductions exceed your available basis and are carried forward indefinitely until additional basis is created. However, if your basis is never restored, these losses may effectively vanish, depriving you of valuable tax benefits. Maintaining a permanent record of suspended losses ensures you can claim them as soon as your basis increases through future profits or contributions.

4. The K-1 Blind Spot

Many shareholders make the mistake of focusing solely on Box 1 (ordinary business income) of their Schedule K-1 when adjusting basis. This narrow view ignores other crucial components, such as tax-exempt income, which increases basis, and non-deductible expenses, which reduce it. Overlooking these items can distort your basis and lead to inaccurate deductions or taxable distributions. A thorough annual review of all K-1 boxes with your CPA ensures that every adjustment is accounted for.

5. The Property Contribution Oversight

Shareholders who contribute property to an S-Corporation often fail to document the transaction properly. Without substantiating the fair market value (FMV) at the time of transfer, the IRS may challenge your basis claim during an audit. This is especially critical for significant contributions such as real estate or equipment. Obtaining professional appraisals and retaining supporting documentation is essential to defend your basis and secure the associated tax benefits.

6. The Debt Basis Time Bomb

Repaying shareholder loans can trigger unexpected taxable income when debt basis has been reduced due to prior losses. Many owners are unaware of this risk and inadvertently create taxable events by accepting repayments without reviewing their debt basis position. Before any loan repayment, it is crucial to evaluate your current basis and plan accordingly to avoid unintended tax consequences.

7. The DIY Tracking Disaster

Perhaps the most avoidable mistake is attempting to reconstruct tax basis years later from incomplete records or memory. The IRS requires contemporaneous documentation to substantiate basis calculations, and without proper records, your claims may be disallowed. Relying solely on memory or outdated spreadsheets is a recipe for disaster. The best practice is to use accounting software with basis tracking capabilities or work closely with a tax professional to ensure accuracy year after year.

2025 S-Corporation Tax Updates & Compliance Tips: What You Need to Know

Key 2025 Filing Deadlines

Timely filing is non-negotiable for S-Corporations. The deadline for filing Form 1120-S and partnerships (Form 1065) is March 15, 2025, with extensions available upon request. Schedule K-1s must be issued to shareholders by March 17, 2025. For individual shareholders, first-quarter estimated tax payments (Form 1040-ES) are due April 15, 2025, while the fourth-quarter estimated payment deadline falls on January 15, 2026. Missing these deadlines can trigger costly penalties — for example, filing Form 1120-S more than 60 days late results in a minimum penalty of $510 or the tax due, whichever is smaller.

New IRS Reporting Requirements

Form 7203 Mandate for Basis Tracking

Starting in 2025, shareholders must file Form 7203 whenever they claim losses, receive non-dividend distributions, sell S-Corp stock, or receive loan repayments from the company. This form ensures accurate tracking of both stock and debt basis. The IRS has intensified enforcement in this area, meaning failure to file Form 7203 can lead to disallowed loss deductions and heightened audit risk.

Schedules K-2 and K-3 for International Activity

S-Corporations with foreign transactions must now file Schedules K-2 and K-3 to report international tax information. These forms provide detailed data to shareholders and the IRS regarding foreign income, credits, and deductions. However, companies with no foreign activity and no shareholder requests may qualify for the “Domestic Filing Exception,” allowing them to bypass these forms.

Tax Law Changes Impacting S-Corps in 2025

Several significant tax provisions affect S-Corporation planning this year. The 20% Qualified Business Income (QBI) deduction under Section 199A is scheduled to expire after 2025, making this year critical for maximizing deductions while they remain available. Bonus depreciation is also phasing down, dropping to 40% in 2025 from 60% in 2024, which may influence decisions on asset purchases. Additionally, new cryptocurrency reporting rules require exchanges to issue Form 1099-DA for digital asset transactions, demanding meticulous record-keeping for S-Corps involved in crypto trading.

State Tax Updates

State-level tax changes also affect S-Corps in 2025. Indiana reduced its flat tax rate to 3%, Iowa shifted to a flat 3.8% rate, and North Carolina lowered its rate to 4.25%. It’s important to note that some states, like Texas, do not recognize S-Corporation status, which can result in dual taxation. Reviewing state-specific filing requirements is essential to avoid surprises.

Basis Tracking and Audit Risks

The IRS continues to focus heavily on basis issues during audits. Stock basis fluctuates annually with income, losses, and distributions, while debt basis applies only to direct shareholder loans. Repaying loans when debt basis has been reduced can create taxable income, a nuance that catches many shareholders off guard. To prepare for potential audits, maintain detailed records including prior-year K-1s, loan agreements, and contribution documentation. If historical basis tracking has been neglected, start reconstructing records now by gathering all available documentation.

Proactive Compliance Strategies

To stay ahead of compliance challenges, leverage accounting software capable of basis tracking, such as QuickBooks with customized features. Conduct an annual review with a CPA to confirm accuracy and ensure Form 7203 is filed correctly. S-Corporations filing 10 or more returns annually must also adhere to the IRS e-filing mandate, making electronic filing essential.

Red Flags to Avoid

Avoid common compliance missteps such as mixing personal and business loans (only direct shareholder loans count toward basis), ignoring tax-exempt income (which still affects basis), and filing late S-Elections. Remember that Form 2553 must be filed within two months and 15 days of the start of the tax year to elect S-Corp status, and missing this window can lead to costly consequences.

CONCLUSION

Navigating S-Corporation tax rules in 2025 requires more diligence than ever. With the IRS tightening reporting requirements — including mandatory Form 7203 filings, stricter basis tracking rules, and heightened audit scrutiny — failing to plan ahead can result in costly penalties and lost deductions. State-level tax law changes and federal updates, such as the phase-down of bonus depreciation and the possible expiration of the Qualified Business Income (QBI) deduction, add even more complexity to the landscape.

The key to staying ahead is proactive compliance. Document shareholder loans thoroughly, reconcile your stock and debt basis annually, and leverage modern accounting tools that simplify reporting. Regular CPA reviews and staying updated on legislative changes ensure that your S-Corp remains tax-efficient and fully compliant.

By addressing these requirements early — rather than scrambling at filing deadlines — you can safeguard your company’s financial health, maximize available tax benefits, and operate with peace of mind knowing you’re fully prepared for IRS scrutiny in 2025 and beyond.