How do money market accounts work? These unique accounts blend the features of savings and checking accounts, offering higher interest rates, easy access to funds, and a secure way to grow your money.”

Introduction (How Do Money Market Accounts Work)

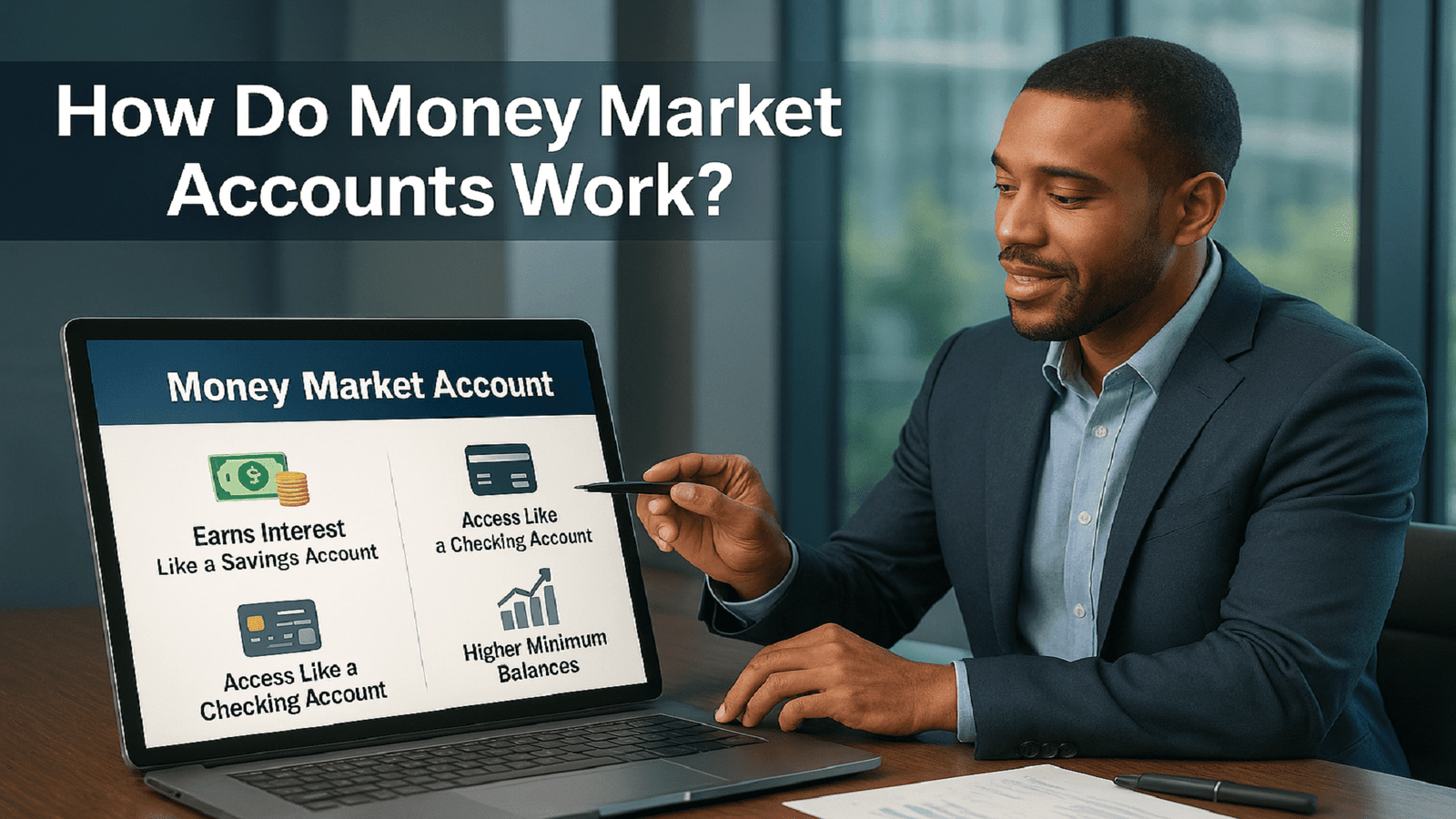

A money market account (MMA) is a unique hybrid banking product that blends features of both a savings account and a checking account. It offers the safety and interest-earning power of a savings account while also providing many of the flexible transaction options of a checking account.

With the best money market accounts, you can make withdrawals, transfer funds, and even use a debit card to make purchases — similar to the convenience of a traditional checking account. At the same time, MMAs often pay higher interest rates than standard savings accounts, allowing your money to grow faster while remaining easily accessible.

However, it’s worth noting that money market accounts may come with minimum balance requirements and monthly transaction limits, so it’s always a good idea to read the fine print before opening one. Still, for those who want both growth and flexibility, a money market account can be an excellent choice for managing savings.

Key Takeaways (How Do Money Market Accounts Work)

- A money market account is neither a checking nor a savings account but has certain characteristics similar to both.

- Like regular checking accounts, money market accounts allow account holders to make withdrawals and transfers, and write checks. They may also allow debit-card transactions and online bill pay.

- Many MMAs offer unlimited ATM withdrawals, but place limits on other types of withdrawals and transfers.

- MMAs, on average, tend to offer higher interest rates than traditional savings accounts but often require higher minimum daily balances.

The best high-yield savings account rates may beat the best money market account rates.

A Short History of Money Market Accounts

Money market accounts — or MMAs — are like the beefed-up version of your regular savings account. They’re built for folks who want their money to do something while still keeping it close at hand. Think of it as the best of both worlds: better interest rates without giving up access to your funds.

But here’s the thing — those perks don’t come totally free. To snag the best interest rates, most MMAs ask for a bit more commitment. You’ll usually need a higher opening deposit and a minimum daily balance, often $1,000 or more. Plus, they often use tiered interest, which means the more you have in the account, the better your rate.

MMAs first took off in the 1980s when interest rates were through the roof. Back then, savers were looking for a low-risk, flexible way to earn solid returns — and money market accounts checked all the boxes.

So, what’s going on behind the scenes? Banks don’t just let your money sit there — they invest it in relatively safe, short-term assets like CDs, government securities, and commercial paper. These investments generate earnings, which is how they’re able to offer you a better return than a standard savings account.

Checking or Savings?

There is often confusion about what exactly a money market account (MMA) is. While it’s not purely a checking account or a savings account, it combines features of both, making it a unique and versatile banking product.

Money market accounts typically provide higher yields than traditional savings accounts, making them attractive to savers who want to earn more interest. They accomplish this by requiring higher minimum balances and sometimes restricting the number of withdrawals or transfers you can make in a given period. These restrictions help banks manage their liquidity while rewarding you with better rates.

Before April 24, 2020, under the Federal Reserve’s Regulation D, both savings account holders and MMA holders were limited to six withdrawals or transfers per month. If you exceeded this limit, you could be hit with penalties or fees. After that date, however, the Federal Reserve lifted this rule, giving banks more flexibility. Still, some banks continue to enforce their own transaction limits and may charge fees if you exceed them.

READ MORE: How Interest Works on a Savings Account

In short, a money market account blends the convenience and transactional capabilities of a checking account with the interest-earning potential of a savings account. It can be an excellent tool if you can meet the minimum balance requirements and manage your withdrawal habits.

Comparison of Checking, Savings, and Money Market Accounts

| Feature | Checking Account | Savings Account | Money Market Account |

| Federally Insured Deposit Account | Yes | Yes | Yes |

| Withdrawals & Transfers Allowed | Yes | Yes, but often limited | Yes, but often limited |

| Allows Debit-Card Transactions | Yes | Sometimes | Sometimes |

| Minimum Daily Balance Requirement | Sometimes | Sometimes | Often |

| Interest Rate Paid | Sometimes (lowest rates of the three) | Yes (typically lower than MMAs) | Yes (typically higher than savings accounts) |

Key Takeaway:

- Checking accounts provide maximum flexibility for daily spending.

- Savings accounts help you grow your money safely with modest interest.

Money market accounts combine higher yields with some spending flexibility, provided you can meet balance requirements and manage withdrawal limits.

The Savings Element of a Money Market Account

Although a money market account shares some features with a checking account — such as check-writing capabilities, debit card access, and easy fund transfers — its true strength lies in its savings power. At its core, a money market account is designed to help you grow your wealth, with your account balance earning interest over time. Typically, the interest rates offered on MMAs are higher than those provided by standard savings accounts, making them an appealing option for savers who want more than the bare minimum.

A key feature of many MMAs is their tiered interest structure. This means the interest you earn is directly tied to how much you keep in the account. Lower balances usually earn a more modest rate, while higher balances unlock higher interest rates, giving you a direct incentive to maintain a larger savings cushion. This tiered approach benefits both banks and customers: it encourages customers to save more while allowing banks to better manage their liquidity and lending operations.

To justify offering these attractive rates, financial institutions often set minimum balance requirements. These minimums can range from a few hundred to several thousand dollars, depending on the bank and the account. If your balance falls below the required threshold, the bank may reduce your interest rate significantly or even charge maintenance fees that can eat away at your earnings.

That’s why it’s crucial to fully understand the terms of a money market account before opening one. Look carefully at the minimum balance rules, the tiered interest rates, and any penalties for falling short. With a solid strategy and disciplined savings habits, a money market account can serve as a powerful financial tool, blending higher returns with easy access to your money.

Pro Tip: High-Yield Savings vs. MMAs

While money market accounts generally offer higher interest rates than traditional savings accounts, it’s important to note that this isn’t always the case — especially if you’re hunting for the absolute best rates on the market.

According to research from Investopedia, many of today’s top high-yield savings accounts actually surpass the highest rates offered by money market accounts. This is largely because online banks and fintech platforms can reduce overhead costs and pass those savings along to customers through higher APYs.

So, if maximizing your interest earnings is your top priority, it pays to compare both high-yield savings accounts and MMAs. Look beyond the marketing and read the fine print about fees, minimum balances, and compounding frequency to find the best option for your financial goals.

✅ FDIC or NCUA Insurance

Most money market accounts are federally insured through the FDIC (for banks) or the NCUA (for credit unions), protecting your deposits up to applicable limits and giving you peace of mind.

✅ Tiered Interest Benefits

Consider MMAs that offer tiered interest rates — these reward higher balances with higher rates, which can be a strategic advantage if you can comfortably keep more money deposited.

✅ Emergency Fund Potential

A money market account is an excellent place to park an emergency fund because it combines higher returns with quick access to your money in case of unexpected expenses.

✅ Fee Awareness

Always review the fee structure. While MMAs can deliver great rates, monthly maintenance fees or penalties for dipping below the minimum balance can quickly offset your interest earnings.

✅ Long-Term Strategy

Think of a money market account as part of a bigger savings plan. It works well alongside checking accounts for spending and high-yield savings accounts for additional savings goals, creating a balanced, flexible financial system.

✅ Rate Shopping

Rates change over time. Periodically review your account’s terms and compare offers from other banks or credit unions to ensure you’re still earning a competitive return.

The Bottom Line (How Do Money Market Accounts Work)

Money market accounts can be an excellent choice for savers who are able to meet higher minimum balance requirements compared to traditional savings accounts. In exchange for maintaining that larger balance, you’ll typically earn a more attractive interest rate, helping your money grow faster over time.

One of the key advantages of MMAs is their flexibility. Many accounts allow you to make withdrawals, transfers, and even perform debit card transactions or pay bills online, much like you would with a regular checking account. This hybrid feature gives you both accessibility and growth potential in one product.

However, it’s crucial to keep in mind that many money market accounts come with limits on the number of withdrawals or transfers you can make during a given period. Exceeding these limits could result in fees or even changes to your account privileges.

If you’re disciplined about maintaining the minimum balance and staying within transaction limits, a money market account can be a powerful tool to grow your savings while preserving easy access to your funds.